Even in Massachusetts’ hot housing market with many homes selling for over $1 million, the vast majority of all home sales will not subject the home sellers to a proposed “millionaire’s tax.” On November 8, 2022, voters will decide on the Fair Share tax which if passed, would create an additional 4 percent tax on taxable income over $1 million to support education and transportation. However, because home sellers are not taxed on the sale price of a home but rather on the capital gain from the sale of a home, most sales will not push them over the $1 million threshold.

Housing Sales and Capital Gains

When a seller sells a home for more than the purchase price, this difference is known as a capital gain (the difference between the sale price and previous purchase price). For example, if a home were initially purchased at $450,000 and eventually sold at $1,000,000, the capital gain would be $550,000. If the same home sold for $1,450,001, the capital gain would be $1,000,001 but the taxable amount of a capital gain from a home sale is almost always reduced by significant deductions (see below).

Would Most Home Sellers Likely Be Subject to the Fair Share Tax?

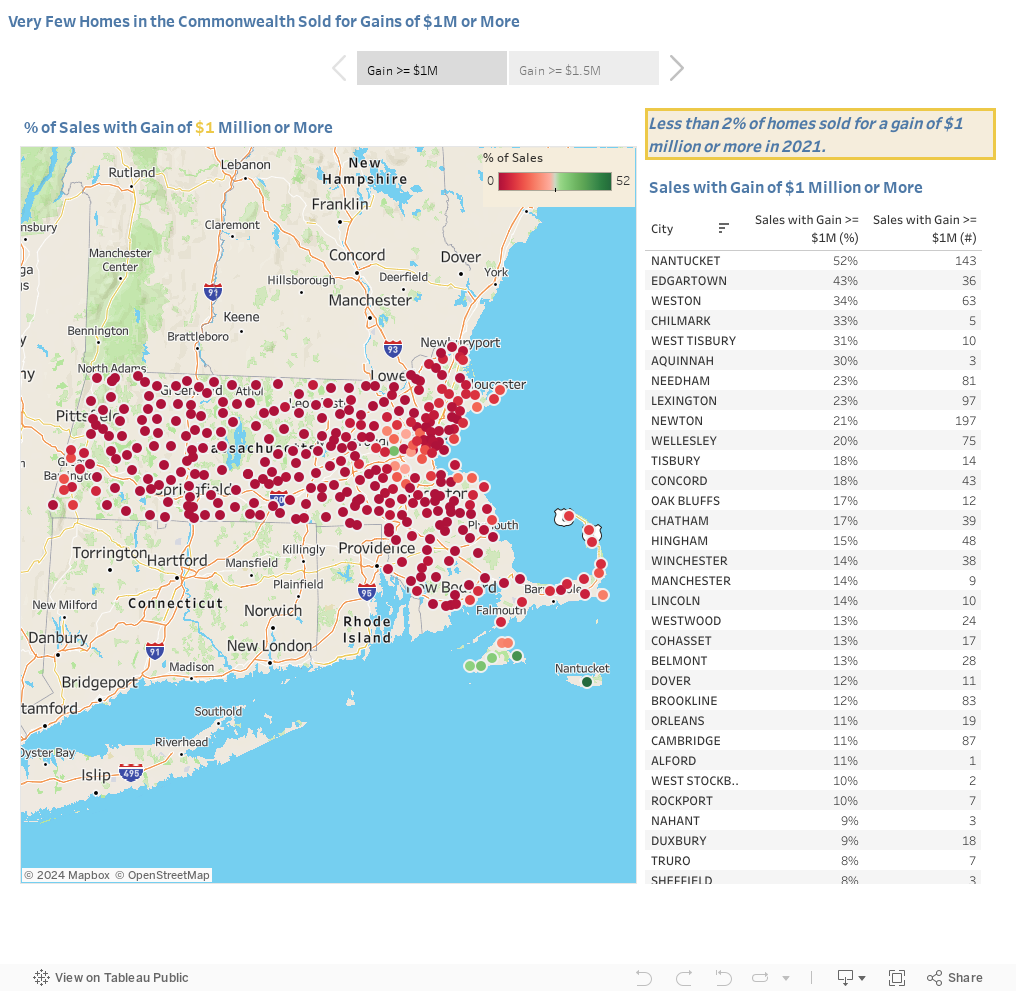

Only a very small portion of households in Massachusetts actually sell a home each year, and most of those sales produce a capital gain of less than $1 million. Even in the current housing market, an analysis of 2021 housing data1 shows that only 2% of all home sellers sold their homes for a gain of more than $1 million.

On top of that, there are several types of deductions home sellers can use to further reduce their taxable capital gain from selling a home. Most home sellers would be eligible for a tax exemption that allows taxpayers to exclude up to $250,000 (or $500,000 if married filing jointly) of capital gains when selling a primary residence.2 With these deductions, most home sellers would need to sell a home for significantly more than $1 million over their previous purchase price before their taxable income reached the Fair Share threshold.3 Even in 2021, a year with rapidly rising home costs and high inflation, less than 1% of all home sales netted the seller a capital gain of more than $1.5 million.4

| 2021 Residential Home Sales in Massachusetts | ||

|---|---|---|

| Capital Gains | Number of Homes Sold | Share of Residential Sales |

| Under $1M5 | 100,448 | 98.0% |

| Above $1M | 2,099 | 2.0% |

| Above $1.5M | 895 | 0.9% |

| Total 2021 Home Sales6 | 102,547 | 100.0% |

| Source: The Warren Group; A Massachusetts-based national real estate and mortgage data provider. Data provided for homes sold throughout Calendar Year 2021. | ||

Footnotes

1The Warren Group; A Massachusetts-based national real estate and mortgage data provider. Data provided for homes sold throughout Calendar Year 2021.

2Commonwealth of Massachusetts. Governor’s Budget Fiscal Year 2023 Recommendations. Personal Income Tax Exclusions from Gross Income. Tax Item 1.021 Exemption of Capital Gains on Home Sales.

3Home sellers realizing gains of $1.5 million (if married) could potentially use the $500,000 capital gains exemption to bring the gain down to $1 million, which is below the Fair Share taxable income threshold

4The Warren Group; A Massachusetts-based national real estate and mortgage data provider. Data provided for homes sold throughout Calendar Year 2021.

5Includes new-built homes and homes sold at no gain or at a loss.

6Includes all homes sold.