During the current legislative session, lawmakers will consider a number of proposals for changing the Massachusetts estate tax. The Massachusetts estate tax is levied on large accumulations of personal wealth as this wealth is transferred from one generation to the next at the time of death. This tax is a source of significant, highly progressive revenue for the Commonwealth, as well as providing other important benefits.

Two proposals are compared here – one put forward by Governor Healey (H.42), and another, S.1784/H.2960, offered in the Senate and House. Both proposals would make significant cuts to the estate tax. Because estate taxes are paid only on the very largest estates each year, any cut to the estate tax is, by definition, regressive – it will make our upside down tax system more unfair. Likewise, due to extreme disparities in wealth between racial groups, any cut to the estate tax will exacerbate racial inequality. The larger the overall cut in estate tax collections, the more economically regressive and racially unequal the results will be. How the cuts are divided between larger and smaller estates also affects economic and racial disparities of wealth.

The Governor’s Proposal

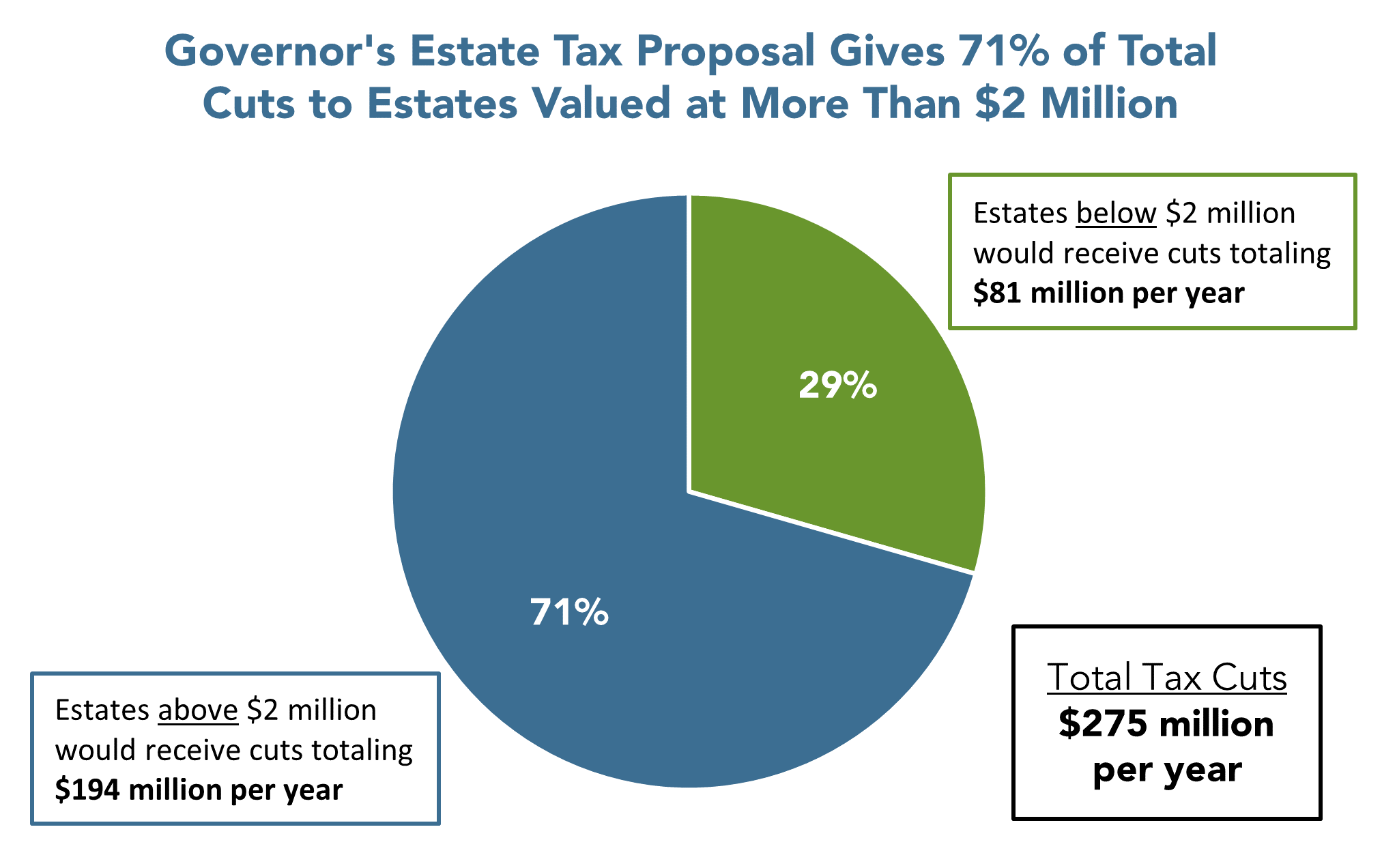

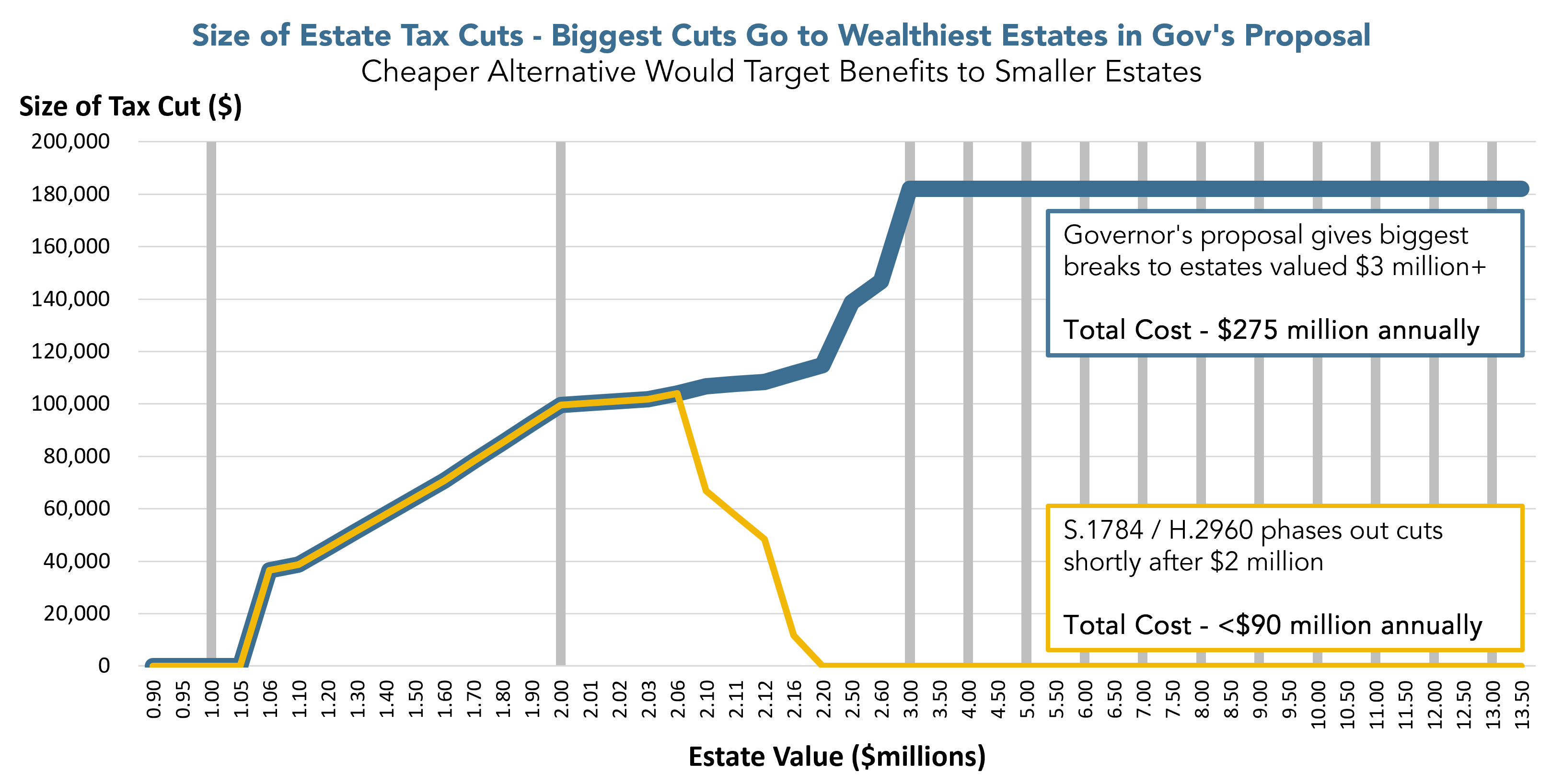

The administration has estimated its proposal (H.42) would result in a loss of $275 million in estate tax revenue each year. This is more than three times the amount MassBudget estimates would be lost under the more modest and targeted proposal in S.1784/H.2960.

The Governor’s plan would eliminate all estate taxes on estates valued at $3 million or less, effectively pushing the estate tax threshold from the current $1 million to a new $3 million level. (Currently, estates valued at less than the $1 million threshold owe no estate tax in Massachusetts.) The Governor’s proposal achieves this result by providing a tax credit of $182,000 against estate taxes owed. Under current Massachusetts law, a $3 million estate owes $182,000 of estate taxes and thus the Governor’s proposed tax credit would zero out the tax liability of estates this size and smaller. Smaller estates, however, can’t utilize the full value of the credit and thus would receive a smaller tax cut. The Governor’s plan does not phase out the value of the tax credit for estates with values above $3 million. Every estate above $3 million in value would utilize the maximum $182,000 tax cut, meaning these largest estates would receive the biggest tax breaks.

One effect of the Governor’s approach is that it eliminates, at very high cost, what often is referred to as the “estate tax cliff”. Under the current Massachusetts estate tax structure, estates just above the tax threshold owe a significant amount of tax while estates just below the threshold owe no tax at all. This abrupt onset of the estate tax can be unsettling for some estate beneficiaries and tax planners. Providing every estate with a large tax break (as the Governor proposes), however, is an unnecessarily expensive way to eliminate the cliff. Many, far less expensive ways to eliminate the cliff are possible. One such solution, which targets smaller tax breaks to the few estates affected by the cliff, is included in S.1784/H.2960.

S.1784/H.2960 “An Act Relative to Estate Tax Reform”

Working from Department of Revenue (DOR) analyses of other, similar proposals, MassBudget estimates that S.1784/H.2960 would cost the Commonwealth less than $90 million a year in lost estate tax revenue. This is roughly a third the cost of the proposal put forward by the Governor, which means S.1784/H.2960 would exacerbate economic and racial inequities less than a third as much as the Governor’s proposal.

S.1784/H.2960 would move the threshold for estate tax liability from the current $1 million to $2 million; estates valued at less than $2 million would owe no estate tax. Department of Revenue estimates provided to the Senate Revenue Working Group last session conclude that shifting the threshold to $2 million would cost the Commonwealth $81 million a year in lost revenue.

In addition to the threshold change, in order to eliminate the “cliff”, S.1784/H.2960 includes a provision that prevents any taxable estate with a pre-tax value above the new $2 million threshold from winding up with an after-tax value below the $2 million threshold. As an example, without this provision, the tax due on a $2,000,001 million taxable estate would be $103,920, which would bring the after-tax value of this estate to $1,896,081. S.1784/H.2960 would limit the tax on this estate to just one dollar, thereby preventing its after-tax value from falling below the $2 million threshold.

The alternative fix to the “cliff” in S.1784/H.2960 is much less expensive than the Governor’s fix because it is much more targeted. The “cliff” impacts only a small number of estates with values just above the tax threshold. The cliff fix in S.1784/H.2960 provides tax cuts only to these few estates and only provides tax breaks big enough to maintain these estates’ after-tax value above the $2 million threshold.

Comparing the Two Plans’ Distribution of Benefits Among Taxable Estates of Different Sizes

While each of these plans would, by definition, deliver tax breaks only to the several thousand largest estates each year, the two approaches distribute these tax breaks very differently among estates of different sizes. Under S.1784/H.2960, all of the tax cuts would go to estates valued at below about $2.2 million, with over 90 percent of the tax cut going to estates of $2 million or less.

Under the Governor’s plan, estates valued at over $2 million would receive more than 70 percent of the much larger tax cut total. As the the Department of Revenue analysis concluded, eliminating taxes on estates below $2 million – a feature of the Governor’s proposal as well as S 1784/H.2960 – would cost $81 million a year. The additional $194 million in revenue that would be lost annually under the Governor’s proposal therefore would go to larger estates, those with values over $2 million.

While both proposals eliminate taxes for estates valued at less than $2 million (the Governor’s proposal eliminates taxes for estates valued at less than $3 million) and both eliminate the “tax cliff”, the Governor’s proposal would be far more expensive. The Governor’s proposal also would be far more lopsided in the benefits it provides, far more economically regressive, and it’s overall impact would be far more racially unequal.